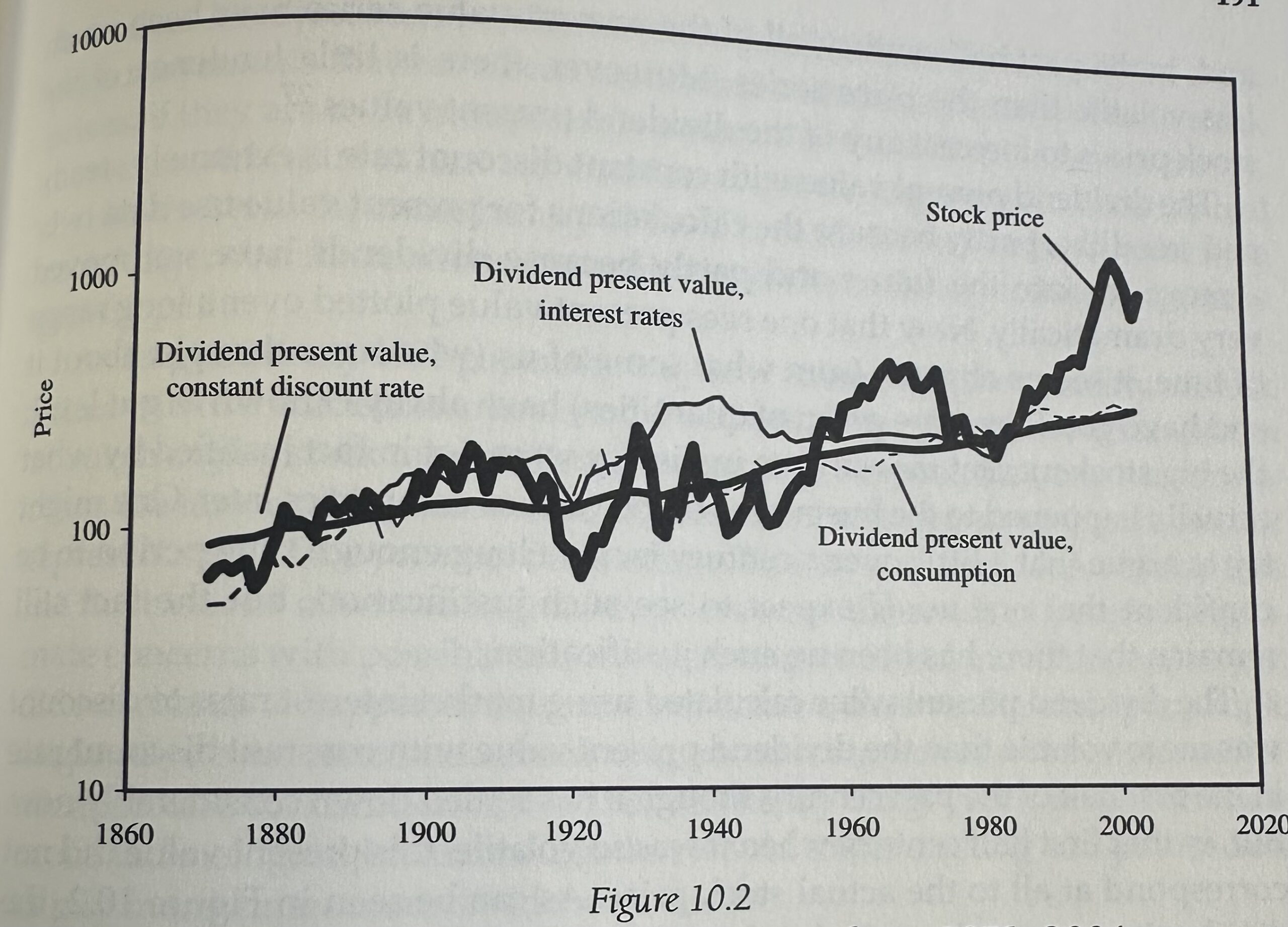

The cash flows move very little. Prices move a lot.

Shiller notes that between September 1929 and June 1932, the real S&P index fell 81%. Real dividends fell just 11%. Between January 1973 and December 1974, the real S&P index was down 54%, while real dividends declined just 6%.

At times, the stock market can act like a lunatic, both to the upside and the downside.

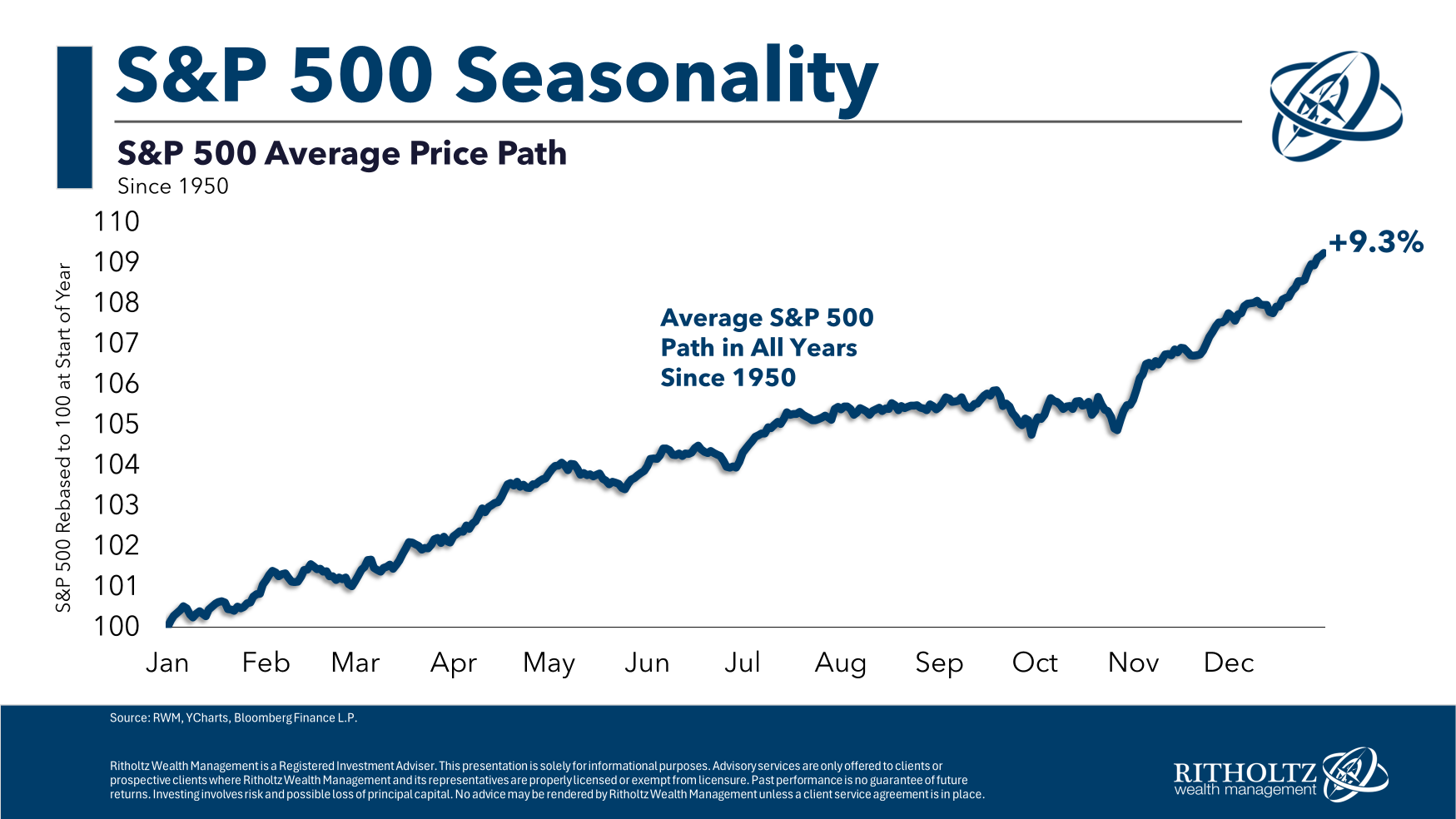

For example, if we took the price performance of the S&P 500 index going back to 1950 for every year and averaged them together, it looks like this:

There are some wiggles here and there but it’s generally moving in the right direction…up and to the right.

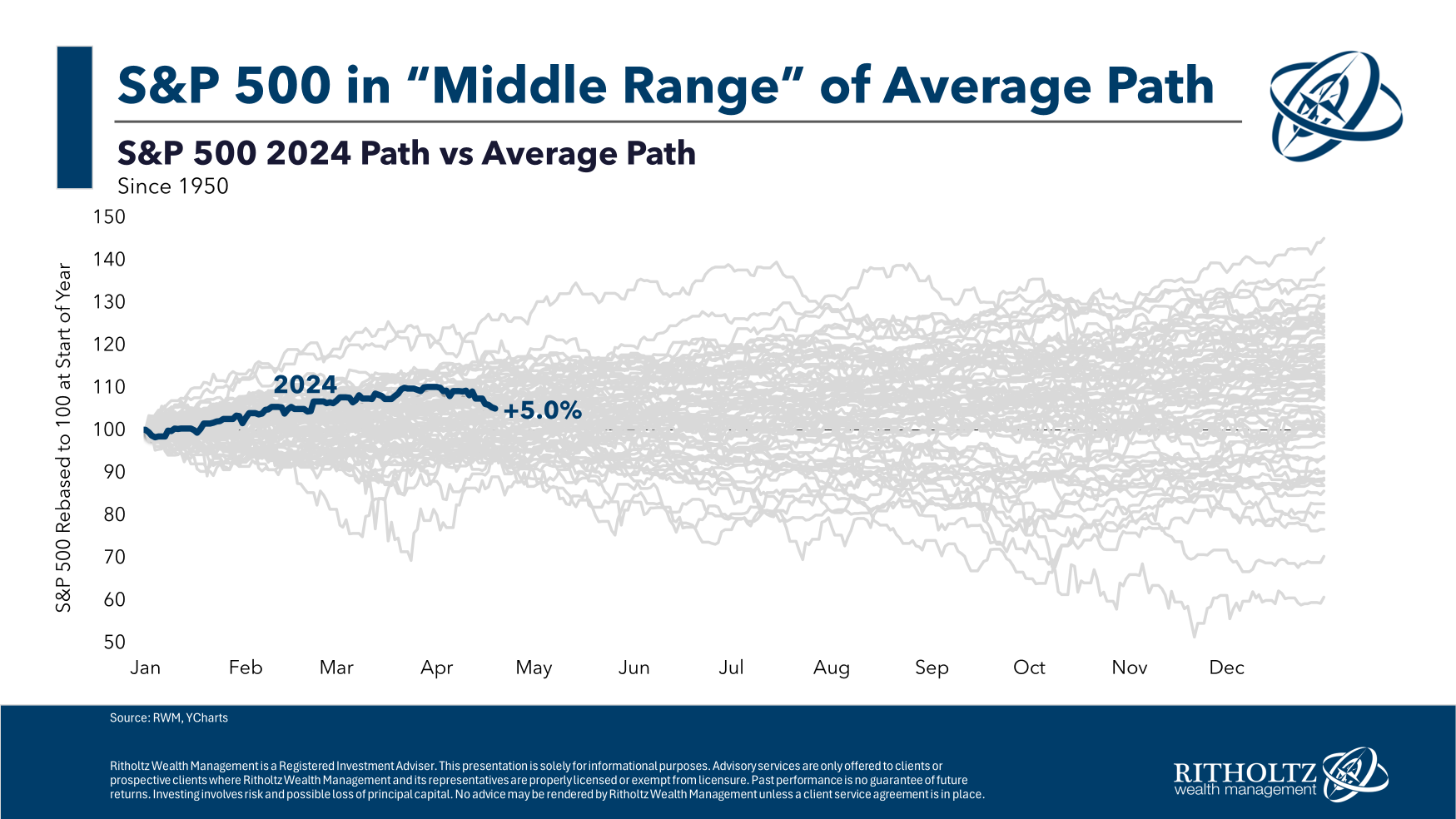

However, if you look at the individual years that make up this average, the range of results are all over the place:

There is no such thing as an “average” year in the stock market.

There can’t be.

You wouldn’t earn a risk premium if stock market returns were predictable.

The volatility is a necessary evil.

I was in New York City this past week so I hopped on The Compound and Friends with Josh, Michael and Art Hogan to discuss “average” years in the stock market and much more:

A Wealth of Common Sense is a blog that focuses on wealth management, investments, financial markets and investor psychology. I manage portfolios for institutions and individuals at Ritholtz Wealth Management LLC. More about me here. For disclosure information please see here.

Get Some Common Sense

Categories

Get a Full Investor Curriculum: Join The Book List

Every month you'll receive 3-4 book suggestions--chosen by hand from more than 1,000 books. You'll also receive an extensive curriculum (books, articles, papers, videos) in PDF form right away.